Members of Davis Health May Be Able to Save on their Home and Auto Insurance

We know quality insurance at an affordable cost is important, that is why we're excited to share our partnership with Blue Ridge Risk Partners. This collaboration is all about ensuring you receive exceptional coverage at competitive rates. For all your personal insurance needs, don't hesitate to reach out to the Blue Ridge Risk Partners family, and experience the outstanding service you deserve.

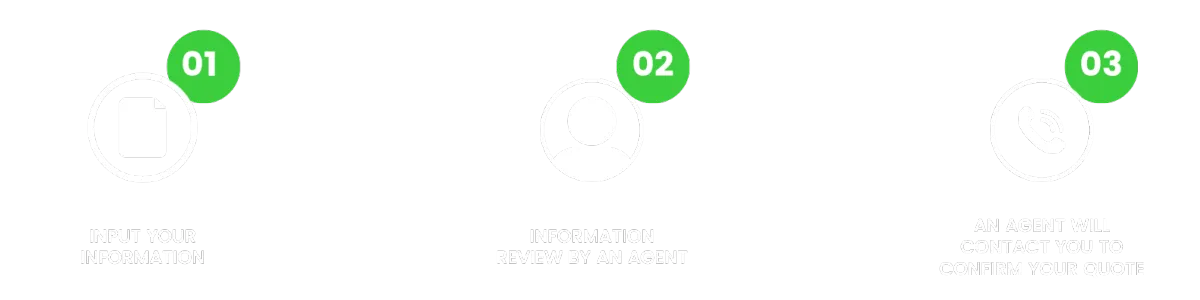

How It Works

____________________________________________________________________________________________________

____________________________________________________________________________________________________

If you prefer a different method of assistance, rest assured that all our members receive personalized support from a dedicated account executive for any inquiries.

Shelia Bailey

Account Executive

304-848-6392

___________________________________________________

The Blue Ridge Way

We are more than just insurance; we are your risk management partners. With access to over 150 carriers and licenses in all 50 states, when you partner with us, you move forward with confidence, knowing that you have secured competitive pricing and comprehensive coverage.

In 2020, three highly regarded and successful independent agencies in the Mid-Atlantic region came together to create Blue Ridge Risk Partners, which has since become one of the top 75 agencies in the United States. This strategic merger enables us to offer innovative products that are advantageous to your organization and its members. The consolidation of our entities has bolstered our capacity for organic growth and strategic partnerships, improved operational efficiency, facilitated investments in cutting-edge technology, and, most importantly, enabled us to offer exceptional products that can better serve your members.

With a presence in 27 offices across Maryland, West Virginia, Pennsylvania, and the Washington D.C. market area, Blue Ridge Risk Partners delivers customized risk management and insurance solutions to over 35,000 clients and counting. We are deeply committed to forging strong partnerships with organizations like yours, providing exclusive products that benefit both your members and your institution.

___________________________________________________________________________________________________

Knowing the Difference Between Term & Whole Life Insurance

Life insurance provides invaluable protection for your family in the event of your death. It ensures the ones you care about can continue to support themselves financially when you are gone. Yet, a recent study by the Life Insurance and Market Research Association reveals that more than half of Americans do not have an individual life insurance policy and 30% have no life insurance coverage at all.

What is life insurance?

Life insurance is a benefit that pays a specific sum of money upon the death of the insured. The benefit is paid to the beneficiary, or beneficiaries, named by the policyholder. The two most common forms of coverage are:

Term life insurance

Provides individual coverage for a specific number of years. The most common terms are 10, 20 and 30 years. If you die within the term of the policy, your beneficiary will receive the full death benefit.

You can often lock in a low premium if you purchase individual coverage when you are young and healthy.

Whole life insurance

Provides a guaranteed death benefit, covers you for your entire life and pays the face value up to the maximum age.

Premiums are higher than you would pay for term life because policies earn cash value and provide you with a substantial death benefit.

Let’s look at how these policies work in more detail.

Term life insurance

Term life insurance is usually the most simple to understand and the most affordable. It provides individual coverage for a specific number of years. The most common terms are 10, 20 and 30 years. If you die within the term of the policy, your beneficiary will receive the full death benefit.

For example, you purchase a $1 million term life insurance policy that provides coverage for 20 years. If you die during year 17 of the policy, your beneficiary will receive $1 million. If you do not die within the 20-year term, your policy may expire and no benefit is paid.

There are three types of term life insurance:

Level term life insurance offers you a fixed premium and a fixed death benefit.

Yearly renewable term life insurance offers you a premium for a year at a time. Your premium will increase as you age, but you may renew your policy without evidence of insurability.

Decreasing term life insurance offers you a fixed premium with a death benefit that decreases over time.

Regardless of which type of policy you choose, there is no savings component, and benefits are paid upon your death.

How much does it cost?

Because you are only purchasing coverage for a specific time, term life insurance is the least expensive of all life insurance options. Premiums are based on the amount of death benefit you purchase and the term of your policy. The insurance company will also consider your age, sex, health and life expectancy.

And, as long as you continue to pay the premiums on time, your policy will remain in force until the end of the term.

What happens at the end of the term?

If you outlive the term of your policy, you will have a few options.

You may renew the policy for another specific term.

You may convert the policy to a whole life benefit.

You may terminate the policy.

Group term life insurance

As mentioned earlier, 60% of employers offer life insurance coverage to full-time employees, according to the Bureau of Labor Statistics. Most of this coverage is provided in the form of a term life policy.

If you have coverage through your employer, your coverage will last as long as you are employed and pay the premium. The death benefit is either a specific dollar amount of coverage (e.g., $10,000) or a multiple of your salary (e.g., 2x base salary). And, it is often guaranteed issue, which means you cannot be denied coverage if you are not healthy.

If you terminate your employment, you may be offered the option to convert your coverage to an individual policy. In most cases, you will not need to provide proof of good health, but your premiums may increase.

Voluntary group supplemental term life insurance

Your employer may offer supplemental term life insurance that goes beyond your group term life coverage. You pay the full cost of this insurance, which is often elected in increments of $5,000 or $10,000, or as a multiple of your salary.

The plan typically offers a specific amount as guaranteed issue (the amount you may purchase without proof of good health). Any amount above that will require evidence of insurability.

Taxes on term life insurance

If you purchase an individual term life insurance policy outside of work, you are paying the premium with money that has already been taxed. As a result, your beneficiaries generally will not have to pay taxes if they receive a death benefit payment. The same is true if you have a term life policy through your employer.

However, the value of your group and supplemental life insurance may be considered part of your income. If you have less than $50,000 of coverage, you most likely do not have any tax liability. If your coverage is valued at more than $50,000, the IRS will set a fair market value and may require you to pay taxes on the difference between that value and the premiums you pay for the coverage.

In most cases, if you have less than $50,000 of group and supplemental term life insurance through your employer, you will not have any associated income taxes. Any group term coverage above $50,000 is assigned a fair market value by the IRS. If you pay less in premiums than this fair market value, the difference is considered part of your income and you would pay taxes on it. Visit the IRS website if you have questions on how the fair market value is calculated.

Whole life insurance

Whole, or permanent, life insurance provides a guaranteed death benefit, covers you for your entire life and pays the face value up to the maximum age.

What differentiates whole life insurance from term life insurance is whole life builds cash value over the life of the policy. A portion of your premium is invested and provides you with a minimum rate of return. The cash value grows tax-deferred; you pay taxes on the value only when it is withdrawn.

Some policies may even offer you the chance to earn dividends. These may be taken as cash or reinvested in your policy to help pay the premium, repay loans or increase the death benefit.

How much does it cost?

Because whole life insurance has a cash value, it is more expensive than term life insurance. Your premium is determined by the amount of your death benefit, age, sex, health and life expectancy. As long as you continue to pay the premiums on time, your policy will remain in force.

Can you borrow money against your whole life policy?

One of the benefits of a whole life insurance policy is your ability to borrow money against the cash value of your policy. Some policies allow you to withdraw this money with no limitation. All you have to do is repay the loan with interest. If you fail to repay the loan, the final payout of your policy is reduced by the outstanding amount.

Taxes on whole life insurance

Whole life insurance benefits are not usually taxable to the beneficiary. However, there are some instances in which the benefit may be taxed. For example:

If you take an early payout on the cash value of the policy, you may be taxed on the amount that exceeds what you have paid in premiums.

If you receive dividends, they may be taxed if they exceed the amount you have paid in premiums.

If you fail to pay back a loan, any outstanding amount may be considered a taxable gain.

If you have questions on how your life insurance policy could be taxed, visit the IRS website.

Comparing term and whole life insurance

When deciding which type of life insurance product to purchase, there is no “one size fits all.” Everyone has their own answer when it comes to choosing how to protect their family from loss of income.

Term life insurance

With term life, you can often lock in a low premium if you purchase individual coverage when you are young and healthy. This may even be cheaper than the coverage offered by your employer. However, if you aren’t healthy or are having trouble purchasing individual coverage, group insurance may be the way to go.

Whole life insurance

If you want to leave a legacy for your beneficiaries, then you might want to consider whole life insurance. These policies earn cash value and provide you with a substantial death benefit.

For more information

If you have questions about how term or whole life insurance can benefit you and your family, talk to your broker or benefits adviser. They can answer your questions, help you determine which type of coverage is right for you and figure out how much coverage you may need to purchase.